WESTCHESTER COUNTY NORTH

OVERVIEW

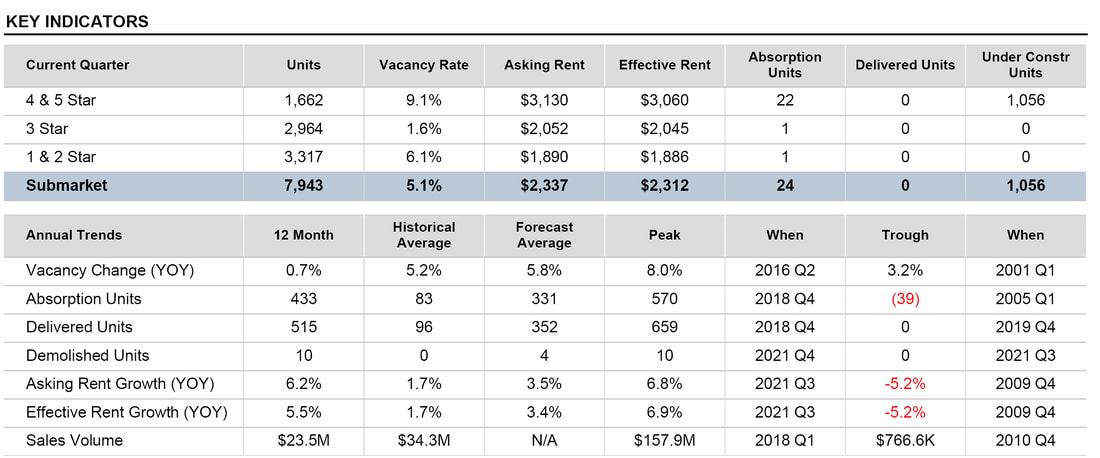

The Westchester County North submarket includes the towns of Port Chester, Tarrytown, Pleasantville, Ossining, and Peekskill. Vacancies here tend to fluctuate as new construction delivers and are typically higher than the metro average.

A notable demand driver here is the accessibility to New York City and the high cost of homeownership in more

in-demand areas of Westchester County. Developers typically plan new projects near Metro-North transit lines which

can offer approximately a 30 to 60-minute commute into Grand Central Station depending on the location within

the submarket.

And while many submarkets throughout New York City witnessed negative annual absorption figures in 2020, this was not the case in the Westchester County North submarket. Still, vacancies remain elevated compared to their long-term historical average at the start of 2022 as the area welcomed an influx of new units over the past year. With demand levels impressing, year-over-year rental growth continues to trend upward as suburban locales continue to witness increased interest from renters.

The submarket's performance in the past year along with the weakness currently facing more dense metro's nationwide is likely the catalyst for why annual sales volume is at its highest total in over a decade. While more than $115 million traded hands in 2020, investment volume has slowed considerably in 2021.

The Westchester County North submarket includes the towns of Port Chester, Tarrytown, Pleasantville, Ossining, and Peekskill. Vacancies here tend to fluctuate as new construction delivers and are typically higher than the metro average.

A notable demand driver here is the accessibility to New York City and the high cost of homeownership in more

in-demand areas of Westchester County. Developers typically plan new projects near Metro-North transit lines which

can offer approximately a 30 to 60-minute commute into Grand Central Station depending on the location within

the submarket.

And while many submarkets throughout New York City witnessed negative annual absorption figures in 2020, this was not the case in the Westchester County North submarket. Still, vacancies remain elevated compared to their long-term historical average at the start of 2022 as the area welcomed an influx of new units over the past year. With demand levels impressing, year-over-year rental growth continues to trend upward as suburban locales continue to witness increased interest from renters.

The submarket's performance in the past year along with the weakness currently facing more dense metro's nationwide is likely the catalyst for why annual sales volume is at its highest total in over a decade. While more than $115 million traded hands in 2020, investment volume has slowed considerably in 2021.

NORTHWEST NEW YORK OFFICE

OVERVIEW

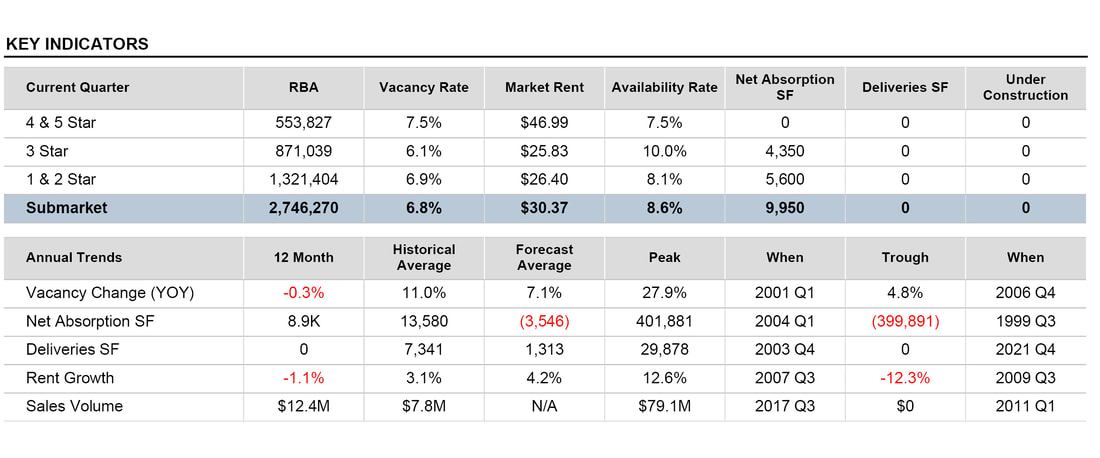

The Northwest Submarket in New York is a midsized submarket that contains around 2.7 million SF of office space. The vacancy rate has been essentially unchanged over the past year, but at 6.8%, the rate was a bit below the 10-year average as of 2022Q1.

The submarket posted 8,900 SF of net absorption over the past year, but on average, annual absorption has been essentially flat over the past five years. Rents fell by 1.1% over the past year. The situation does look better on a longer timescale, however, as rents have posted a solid average annual gain of 1.8% per year over the past decade.

There are no supply-side pressures on vacancy or rent in the near term, as nothing is under construction. Moreover, the inventory has actually contracted over the past 10 years, as demolition activity has outpaced new construction.

Office properties traded with regularity last year, consistent with the generally high level of activity over the past

three years.

The Northwest Submarket in New York is a midsized submarket that contains around 2.7 million SF of office space. The vacancy rate has been essentially unchanged over the past year, but at 6.8%, the rate was a bit below the 10-year average as of 2022Q1.

The submarket posted 8,900 SF of net absorption over the past year, but on average, annual absorption has been essentially flat over the past five years. Rents fell by 1.1% over the past year. The situation does look better on a longer timescale, however, as rents have posted a solid average annual gain of 1.8% per year over the past decade.

There are no supply-side pressures on vacancy or rent in the near term, as nothing is under construction. Moreover, the inventory has actually contracted over the past 10 years, as demolition activity has outpaced new construction.

Office properties traded with regularity last year, consistent with the generally high level of activity over the past

three years.